Pay Yourself First!!! Then Enjoy the Free Money!!

I wanted to share how I’ve adjusted my investment strategy. Since I won’t have access to real estate for a few years, I’ve had to pivot — and that’s okay. We’ll figure that part out when the time comes. For now, I’ve decided to focus on a dividend-based investment plan and enjoy the cash flow along the way.

The idea of “paying yourself first” works like this: invest in something a bit more conservative when you’re starting out, at least until you hit your first $100K. At the moment, I’m mainly investing in dividend-focused ETFs. Right now, I’m mostly in JEPI, but back in 2022 I researched and built out a five-fund dividend strategy (I’m no expert, but at the time, these five seemed solid to me):

JEPI

VIG

SCHD

SPHD

DIVO

I still want to research whether there’s a good dividend-focused energy fund to add to the mix, but I haven’t dug into that yet.

That was the structure I envisioned for my dividend play.

What I do now is pay myself $1,000 per month into this account. You can absolutely start smaller — even $250 per month into a single ETF if that’s where you are. The key is consistency.

I’ve basically promised myself that this will be my personal “fun” account — the one that generates income and momentum while I rebuild and get fully back on track.

Here’s how I divide the dividends:

50% goes right back into the fund (reinvestment).

The engine keeps growing on its own, helping it keep up with the 4% rule and inflation.

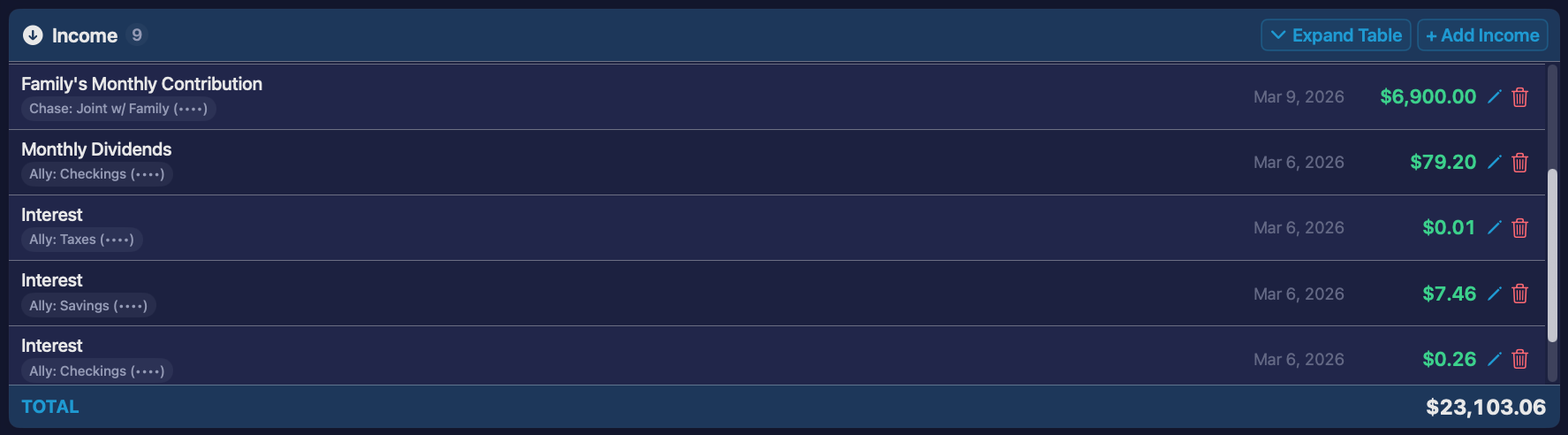

This month, I was able to generate around $180 in dividends (and yes — do you like the new UI for my budget app? I updated it).

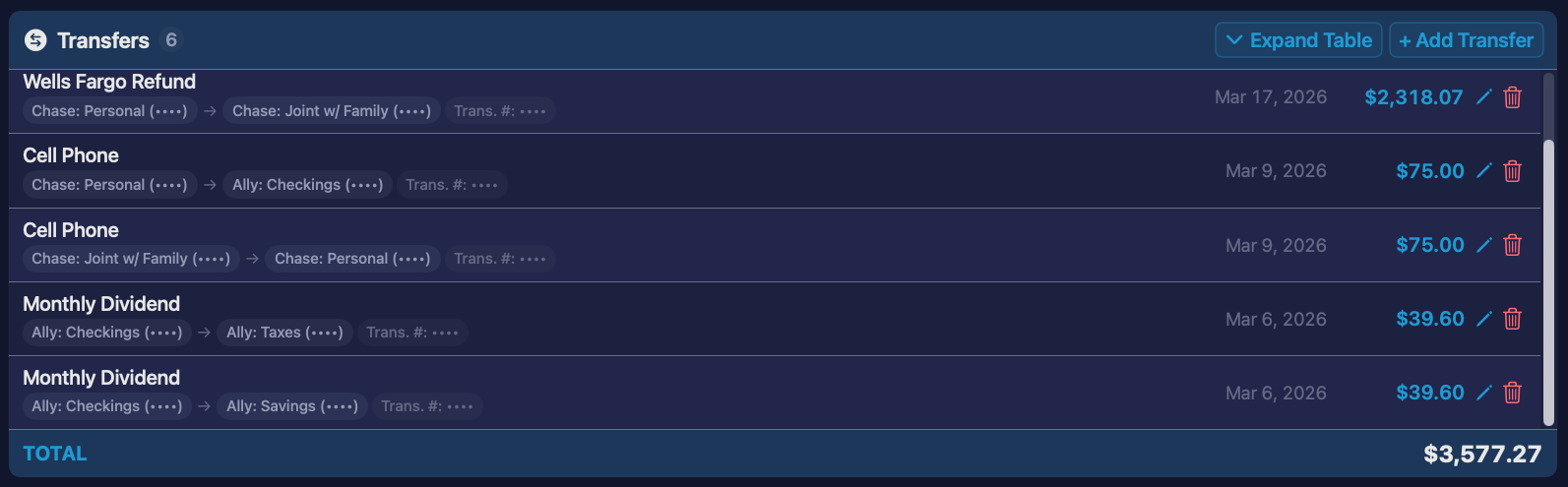

I kept a little over half to reinvest back into the account and took $79.20 as my monthly dividend payout.

The reason I reinvested slightly more than half is because I prefer to buy whole shares of JEPI, and at this stage, I’d rather lean toward saving more than less.

25% goes into my tax account.

I stay ahead of taxes as much as possible (don’t go to jail over it 🙂).

If you don’t end up owing the government anything at the end of the year, that money can feel like free cash flow.

Another 25% goes into my “fun” account — or, more realistically right now, into your savings account to build your emergency fund to where it should be.

The idea is that you still get to enjoy some of the cash flow along the way.

However, at this stage (and probably for a while), my emergency fund is lower than I’d like, so that portion is going there for now.

The goal, at the end of the day, is to have this replace my paycheck one day. It’s going to take a LONG time, but little by little is the name of the game.