Step 3: Income! (but pay yourself first ALWAYS)

Alright, let’s move on to everyone’s favorite part of the budget… INCOME!!!

When you get paid — whether it’s your paycheck, money a friend pays you back, interest from your bank accounts, dividends from your stocks — EVERYTHING needs to be tracked. You need to know exactly where you stand in your financial spectrum at all times.

I know it sounds like a pain, but this is the balancing act to your expense tracking. The good news? Income tracking is actually simpler. Most of the time, all you’re doing is dumping it into your main spending account and then dividing it into 3–4 different accounts or “buckets” to keep everything aligned.

But let’s break it down.

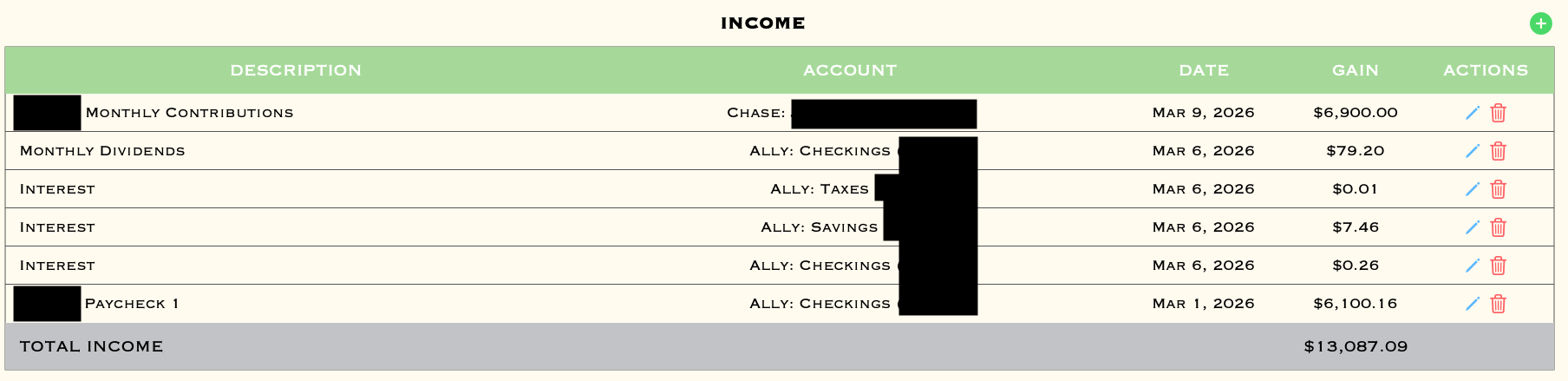

OK, on the right is my income table. It’s March 9th, and I run my budgets on a monthly basis. So I still have about 70% of the month left to log other sources of income, including my second paycheck and anything else that comes in.

But like I said — even the entry with a single penny should be tracked. Everything counts. (On a side note, I’m actually happy we’re getting rid of the penny as physical currency, but that’s a different story.)

The “Monthly Contributions” you see are from my family for the family properties. Like I mentioned before, I help manage those properties, so I don’t count that money as part of my personal net worth since it’s shared. However, because I oversee the account, I still track it in my budget.

Income tracking is much simpler than expenses because most of us don’t get paid that frequently, and friends don’t usually pay you back every day. But even if it’s slow or irregular, keep it all here. It’s important.

There’s not much to say here but you need to track your income as well. Next step will be to use both the Expenses and the Income to see what you truly have in your bank account for any given day. I mean it’s a simple add here and subtract there, but it all matters when keeping your money organized.

NOTE: PAY YOURSELF FIRST!!!!

I’ll make a separate article about this later, but you should always pay yourself first from your paycheck. We’ll come up with some sort of equation when we get there. 🙂

Whether you’re working at In-N-Out or anywhere else, always save a chunk of your paycheck for yourself. Even if it’s just $100, it’ll be worth it in the end and in the long run.

It also helps you build that investment and savings muscle. JUST do it. Even if it’s something as small as $100.

In this day and age, that’s like eating McDonald’s three times a month. Come on. Get out of here. MEAL PREP.